Travel Goods Industry Navigates Change: What the 2025 Market Report Reveals

The full 2025 Market Report is featured on page 38 in the Winter 2025 Issue of the TGA Magazine.

The U.S. travel goods industry is in the midst of a complex, transition-heavy chapter — marked by shifting consumer behavior, rising global travel, and continued price pressure across every major product category. The 2025 Market Report explores these changes with a data-driven look at how the market has evolved from the post-pandemic surge to today’s more measured demand.

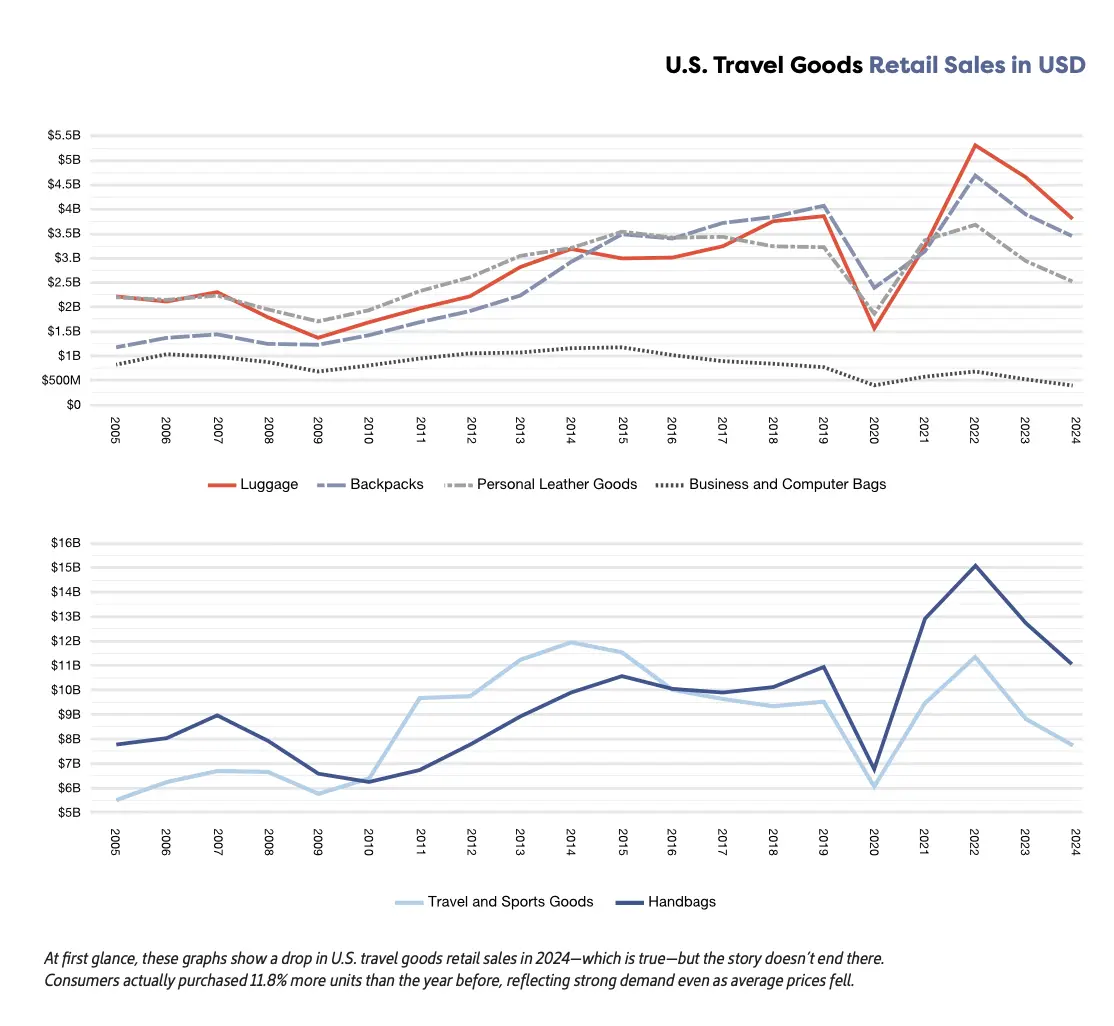

After travel goods sales surged in 2022 — with volume rising 28% from 2.2 to 2.8 billion units — the market cooled significantly. Sales by value dropped -17.1% in 2023, and the downward trend continued into 2024. The industry saw overall retail value fall 15.3%, landing at $28.4 billion — down from $33.6 billion in 2023 and even below pre-pandemic 2019 levels.

But there's a lot more happening than just a drop in sales. As the report highlights, “U.S. consumers bought 11.8% more travel goods than the year before—proof that demand is still strong.” Lower prices across categories fueled higher unit sales, even as inflation and shifting spending patterns reshaped what consumers purchased and why.

Here’s a quick look at how TGA estimates each of the major travel goods categories performed in 2024:

-

Luggage: After booming in 2022 and 2023, sales fell 19.9% by value and 2.6% by volume in 2024 as average unit prices dropped 17.8%.

-

Backpacks: Despite a 12.6% decline in value, volume rose 7.1% as prices fell 18.4%.

-

Travel/Sports Bags: Value dropped 13.9%, but volume surged 14.8%, with unit prices falling 25%.

-

Business Cases/Computer Bags: A long-term category decline continued, with sales down 29.9% by value and 7.1% by volume.

-

Personal Leather Goods: Value slid 15.7%, while volume rose 2.7% as consumers moved toward digital alternatives.

-

Handbags: The category fell 14.8% by value and 19.4% by volume, driven largely by inflation and shifting consumer priorities.

The report also traces how factors like tariffs, supply chain pressures, and the lapse of the Generalized System of Preferences (GSP) contributed to higher costs that reshaped pricing in 2022 and beyond.

Despite these challenges, the data shows clear signs of resilience. Consumers are still buying — they’re simply buying differently. Categories tied to mobility, convenience, work-life flexibility, and post-pandemic routines continue to evolve as prices stabilize and the market finds its post-surge rhythm.

Read the Full 2025 Market Report in the Winter 2025 Issue of the TGA Magazine

This preview only scratches the surface. The full article breaks down how each category is performing compared to previous years, what’s driving price declines, how inflation is reshaping purchasing behavior, and what these shifts mean for brands, manufacturers, and retailers in 2025 onward.

Read the full report here on page 38 in the Winter 2025 Issue of TGA Magazine.